Nov 13 2006

Most of us can still remember the 1997 economy crisis which hit Asian started from Thailand’s Baht (hence known as Asian currency crisis) being dumped by investors. Central Bank of Thailand tried to intervened but later it was let go for a freefall as its’ equivalent to catching a falling knife. It then affected not only currency but stock markets and other asset prices (such as property) in Asian Tigers countries. Countries affected – Indonesia, South Korea, Malaysia, Hong Kong, Laos, Philippines. Mainland China, Taiwan, Singapore and Vietnam were “relatively” unaffected. But all these countries saw their currencies dived to a level never seen before against the US dollars.

Until 1997, the economies of Southeast Asia was the main attraction of FDI (foreign direct investment) due to its’ high interest rate. The hot-money pumped into this region jacking asset prices such as buying power, properties and stocks and so on. It seems these countries are invincible. GDP growth rate of 8 – 10 % is normal for these countries.

Until 1997, the economies of Southeast Asia was the main attraction of FDI (foreign direct investment) due to its’ high interest rate. The hot-money pumped into this region jacking asset prices such as buying power, properties and stocks and so on. It seems these countries are invincible. GDP growth rate of 8 – 10 % is normal for these countries.There were claims that this 1997 crisis was triggered by events in Latin America (Mexico peso crisis in 1994) after which investors lost confidence and started to pull money out from Southeast Asia. The Prime Minister of Malaysia during that time, Mahathir on the other hand blamed it on currency speculators such as George Soros (who used to be his good friend before this).

However there was research done before the crisis that pointed the “Miracle” of economy of Southeast Asia was the result of the influx of huge capital investment. Furthermore countries such as Indonesia, Thailand and South Korea policies encouraged external borrowing and hence led to excessive exposure to foreign exchange risk. Another factor could be the recovery of U.S.’s economy after recession in 1990s leading to rising of interest rates to head off inflation. With higher interest rate, U.S. becomes more attractive for investors who decided to pull out money parked in Southeast Asia back to U.S.

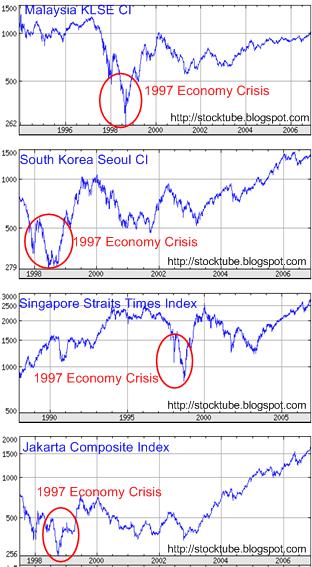

Fast forward – from the chart attached, it can be seen most of the affected countries have recovered. In fact most of them are performing better than during crisis with the exception of Malaysia. South Korea which accepted assistance from IMF and went through a very bitter cycle of recovery can stand proud of their achievement today. Indonesia has performed equally well, with the latest news of it attracting more FDI than Malaysia. What is the problem then with Malaysia’s turtle pace of recovery?

Many economists agreed that a country needs to have a strong, transparent and correct information about macroeconomic policies in order to attract confident foreign investors for long-term investment. Without which, the country will need miracle to sustain and grows its’ own economy.

Hence, is the current Bursa Malaysia Composite Index (KLCI) which has breached 1,000 points and recorded 7-years high is here to stay ? Or is it being played up due to the coming UMNO election ? Or the possibility of a General Election is around the corner ? It could be the year-end window-dressing is early this year. Nevertheless it’s a known fact that most of the index-linked stocks are majority owned by several government bodies such as EPF, Tabung Haji, PNB etc. To move TMT (Telekom, Maybank, Tenaga) stocks is equivalent to move the Composite Index. Hence I would still wait and see if this can sustain for the months to come. Note that resistance is at 1,250 level.

|

|

November 13th, 2006 by financetwitter

|

|

|

|

|

|

|

Comments

Add your comment now.

Leave a Reply