When people talk about tycoons, you can’t float too far away without taking a hard look at shipping industry. Pre-technology age, building an empire (always associated with shipping) was a hard work which not only required huge resources but also tons of precious time. Shipping tycoons such as Y.K. Pao, Robert Kuok, Li Ka-shing, the late “Godfather” Henry Fok Ying-tung and even former Hong Kong Chief Executive Tung Chee-hwa built or inherited their wealth from shipping business, one way or another.

And so, when former premier Mahathir tried to create his own shipping tycoon in the form of none other than his son, Mirzan Mahathir, it raised everyone’s eyebrows. Public quietly accept while oppositions cried the model of nepotism or favoritism. The economy was booming and the stock price of Mirzan’s new pet Konsortium Perkapalan Bhd (KPB), now known as Konsortium Logistik Berhad (KLSE: KONSORT, stock-code 6157), skyrocketed to market capitalization exceeding RM2.5 billion.

The jolly good time didn’t last, the 1997 Asia Economy Crisis hits and the glory of KPB was reduced to a pile of dust and debts estimated at RM1.8 billion. KPB was on the brink of bankruptcy and Petronas (the state oil giant) was roped in to purchase (bailout) KPB’s shipping assets at a mind-boggling US$220 million. Such scenario goes to show that the business needs real shipping acumen in order to stay afloat else you’ll sink faster than the Titanic.

Knowing Shipping Terminology

Lately you heard of how shipping stocks are doing well due to some bombastic language such as Baltic Dry Index, Baltic Clean Tanker Index and Baltic Dirty Tanker Index. Just like energy-related stocks rely on the daily global oil price and telecommunication relies on ARPU (average revenue per user) as its measurement of business, shipping industry has its own terminology as well.

The Baltic Clean Tanker Index measures the cost of carrying refined oil products while the Baltic Dirty Tanker Index is the yardstick for crude oil. Both indexes however have nose-dived. However Baltic Dry Index (BDI) is another totally different animal – today’s (24th Sept 2007) BDI is trading at 9,082.00. BDI’s number changes everyday and depends on London-based Baltic Exchange. Basically the exchange is the common area where all the brokers around the world will spell out the booking cost for various cargoes of raw materials on various routes. Together with speed and type of ship plus the estimated time-frame of a voyage, it produces the BDI.

The Baltic Clean Tanker Index measures the cost of carrying refined oil products while the Baltic Dirty Tanker Index is the yardstick for crude oil. Both indexes however have nose-dived. However Baltic Dry Index (BDI) is another totally different animal – today’s (24th Sept 2007) BDI is trading at 9,082.00. BDI’s number changes everyday and depends on London-based Baltic Exchange. Basically the exchange is the common area where all the brokers around the world will spell out the booking cost for various cargoes of raw materials on various routes. Together with speed and type of ship plus the estimated time-frame of a voyage, it produces the BDI.

Bulk container carriers specifically carry unfinished goods such as building materials, cement, grain, coal, iron ore and so on. BDI is probably the most reliable and honest indicator of the economy simply because people don’t book freighters unless they need to move cargo around the globe. But the argument is always that the bullishness in BDI is merely due to China’s huge appetite for raw materials.

MAYBULK Fundamentals

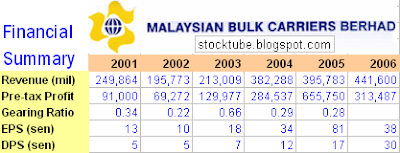

Malaysian Bulk Carriers Berhad (KLSE: MAYBULK, stock-code 5077) is probably one of the shipping stocks preferred by most investors. While players such as Halim Mazmin Berhad (KLSE: HALIM, stock-code 7102) and Malaysian Merchant Marine Berhad (KLSE: MMM, stock-code 7040) found the hard way that the business is not as rosy as it looks after registered losses, MAYBULK is enjoying consistent and excellent business. MAYBULK’s main focus is in the bulker and tanker segment. Together with 70% of its vessels actively participating in spot charter market, the strategy works like a charm. Although spot charter market gives higher returns, the charter periods are shorter hence creating the idle-time for vessels. However with the correct formula of mix and match to maximize the utilization, MAYBULK’s profit continues to grow. Based on info from its website, the company has 12 Bulk Carriers, 4 tankers and 1 new ship to be delivered in Oct 2007.

MAYBULK’s main focus is in the bulker and tanker segment. Together with 70% of its vessels actively participating in spot charter market, the strategy works like a charm. Although spot charter market gives higher returns, the charter periods are shorter hence creating the idle-time for vessels. However with the correct formula of mix and match to maximize the utilization, MAYBULK’s profit continues to grow. Based on info from its website, the company has 12 Bulk Carriers, 4 tankers and 1 new ship to be delivered in Oct 2007.

To a certain degree having tycoon Robert Kuok as its boss has its advantage. His very-close relationship with China government helps in the business of transporting goods such as coal and iron core which is expected to be up by 9.4% in 2007. For the first half ended June 30, 2007, the company recorded a higher pre-tax profit of RM288.571 million compared with RM143.341 million in the preceding period of last year. Its revenue was also higher at RM253.555 million from RM215.727 million previously while registered net profit of RM129.47 million, an 84.7% increase compared with RM70.11 million in 2Q06.

To a certain degree having tycoon Robert Kuok as its boss has its advantage. His very-close relationship with China government helps in the business of transporting goods such as coal and iron core which is expected to be up by 9.4% in 2007. For the first half ended June 30, 2007, the company recorded a higher pre-tax profit of RM288.571 million compared with RM143.341 million in the preceding period of last year. Its revenue was also higher at RM253.555 million from RM215.727 million previously while registered net profit of RM129.47 million, an 84.7% increase compared with RM70.11 million in 2Q06.

MAYBULK has been recording good and sustainable profit and has been paying good dividend. In fact it had paid double-digit in terms of cents per share since 2004, with 2006 registered the highest dividend yield or 30 cents per share. Revenue has been on uptrend since and market analysts are estimating another record dividend for the year 2007.

Technical Reading from Chart

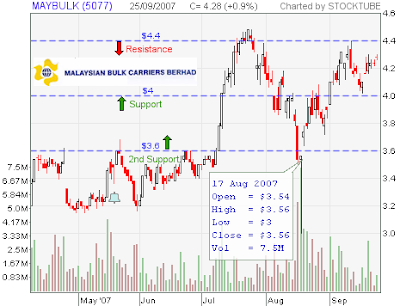

Since MAYBULK breached the resistance level of RM3.60 on 9th July 2007, it has never look back. Thereafter the stock actually has been trading within the wave-range of RM3.60 – RM4.40 and the middle value of RM4.00 has been established as the support/resistance level. Hence, for stock tr

Hence, for stock tr

aders, you can actually buy in stages at both RM4.00 level and if this level is breached, buy in another stage at RM3.60 level. The support of RM3.60 should be strong looking at how the stock rebound after 17th Aug 2007 with very high volume. Unless something really bad happen, there’s no justification for the stock to trade below RM3.60 level. Nevertheless with current record level of BDI, it is a dream if you wish to scope at this level.

What analysts said about MAYBULK?

AmResearch said dry-bulk rates were expected to rise further for two more years and it likes Maybulk for its sound manage and has a “Buy” call on the stock with target price of RM5.15 per share. OSK has forecast MAYBULK raking in as much as RM526.3mil in net profits on the back of RM517.2mil in revenue for the financial year ended December 2007. OSK has a fair value of RM4.88 based on MAYBULK’s 11 times price-earnings ratio.

When to jump into the vessel?

To stay afloat, you should trade based on the indicators from the technical chart – to maximize profit. Nevertheless the fundamental is strong and if you wish to long now believing the stock will jumps above RM4.40 comes the next earning announcement, nobody can stop you really. Alternatively you might want to study Swee Joo Berhad or Hubline Berhad as the shipping stocks (I’ll leave that as another discussion at another time). As part of the best practice in stocks investing, diversification is the name of the game and you should seriously consider a transportation stock in you portfolio. What better stock than MAYBULK which has the support of Robert Kuok?

|

|

September 25th, 2007 by financetwitter

|

|

|

|

|

|

|

Comments

you’re right benjamin that maybulk periodically made extraordinary gains from sale of its vessels …

on the contrary, it’s a good move to “capitalize” on high vessel price when the management can foresee a softer freight rates in certain type of vessels in near future …

that’s why the 2005 financial year recorded more than RM400 million from the sale of its 3 bulk carriers and 4 panamax tankers … to build a new ship will takes about 2-years and if there’s a demand from another shipping co which couldn’t see a softer rate but need a vessel in a hurry, why not sell your existing vessel for good profit if you can see what’s coming?

furthermore, maybulk do not sell vessel for the sake of selling it … only if the profits outstretch the risks of potentially having an idling vessel will the management make the decision to sell it … don’t forget at the same time maybulk could be expecting a delivery of its own new ship …

so in my opinion the question of shortage of ships to take care of engaged charters does not arise … making profit from charter is still the bread and butter of maybulk … it’s a matter of how to optimize the usage and how to maximize profit and reduce the operating cost during low freight rate period …

that’s why you see how MMM and Halim is in red … of course having robert kuok play a role as he might be able to tell in advance the demand from china …

cheers …

Goodday,

But I thing I noted that the recent profit not really come from day to day operation but rather selling off bulk vessel.

If a company continuously selling off the vehicle they used to run day to day business. The long term earning ability certainly will be affected. This is just my 2 cent concern.

Nonetheless, I am still holding maybulk shares. No doubt the price hike and dividend yield is really impressive. ^_^